Compliance and Corporate Governance

Foreign companies that operate through a branch in Brazil need more than market knowledge and commercial ambition. They need a clear structure for compliance and corporate governance capable of connecting headquarters’ expectations with Brazilian legal, tax, regulatory, and operational requirements. For foreign investors, this is especially important because a branch is not merely a sales presence or a commercial extension. It is a formal corporate structure that must interact with Brazilian authorities, maintain records, appoint representatives, and demonstrate that decision-making is properly documented.

In Brazil, the opening and maintenance of a foreign company branch involves authorization and corporate registration procedures. The official Brazilian government service portal states that authorization for acts involving a branch of a foreign business company is handled through the competent federal structure, and the Department of Business Registration and Integration, known as DREI, presents itself as the body responsible for matters involving foreign companies authorized to operate in Brazil. This means that governance begins before operations start, because the company must define who will represent it, how corporate acts will be approved, and how the Brazilian branch will remain aligned with headquarters.

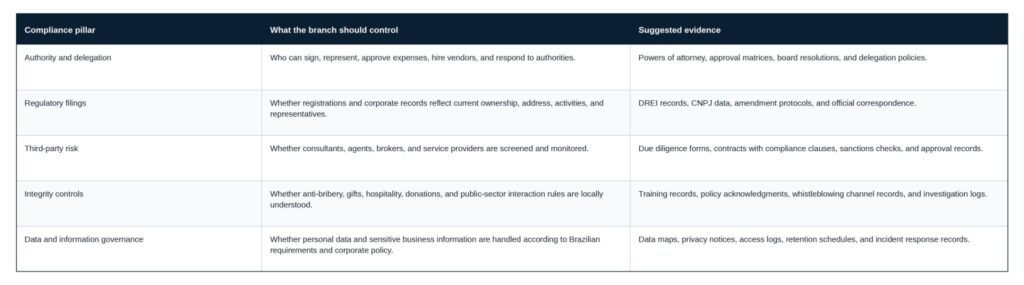

A well-governed branch should operate under a documented chain of authority. This includes the powers granted to the legal representative, the internal approval matrix, the limits for signing contracts, and the process for reporting material matters to the parent company. For foreign investors, these controls are not bureaucratic details. They are safeguards that reduce the risk of unauthorized commitments, inconsistent filings, delays in corporate updates, and uncertainty when local authorities request information.

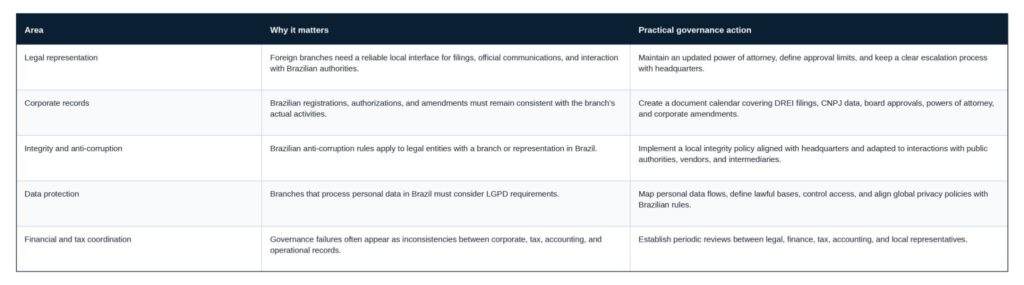

The first pillar of governance is legal representation. A foreign company branch typically depends on a local representative or attorney-in-fact to receive communications, sign documents within the authorized scope, support filings, and coordinate interactions with authorities and service providers. The governance risk is not simply whether someone has been appointed, but whether that person’s powers are current, properly drafted, and consistent with the parent company’s internal controls. A power of attorney that is too broad may create exposure, while one that is too narrow may delay essential filings or commercial actions.

The second pillar is corporate record control. Foreign branches should maintain accurate and updated records relating to their authorization, registration data, representatives, addresses, corporate documents, amendments, and business activities. The Brazilian Federal Revenue Service requires legal entities and certain foreign entities to be identified through tax registration mechanisms, including the National Register of Legal Entities, known as CNPJ, depending on the case and activity. Because of this, governance should include periodic checks to ensure that corporate records, tax records, accounting records, and actual operations remain consistent.

Compliance also plays a central role in the way foreign branches interact with public authorities, vendors, commercial partners, and intermediaries. Brazil’s Federal Decree No. 11,129 of 2022, published by the Presidency of the Republic, regulates aspects of the Brazilian Anti-Corruption Law and describes integrity programs through elements such as commitment from senior management, standards of conduct, training, risk analysis, accounting controls, reporting channels, disciplinary measures, and due diligence for third parties. For a foreign company branch, this means that a global compliance policy should not simply be copied into Brazil without adaptation. It should be translated into local controls that reflect the branch’s real exposure.

A practical compliance framework should also consider third-party risk. Many foreign companies entering Brazil work with consultants, commercial agents, accounting firms, legal representatives, logistics providers, brokers, and local advisors. These relationships can be essential, but they can also become risk points if due diligence, contract clauses, approval records, and monitoring routines are weak. The Office of the Comptroller General of Brazil, known as CGU, published guidance for private companies on integrity programs in 2024, emphasizing risk-based measures, commitment from leadership, internal controls, reporting mechanisms, and continuous improvement. This guidance reinforces that compliance should be an operating system, not a document stored after incorporation.

Data protection is another governance issue that foreign branches should not overlook. Brazil’s General Data Protection Law, Law No. 13,709 of 2018, published by the Presidency of the Republic and also made available through the National Data Protection Authority, applies to the processing of personal data in circumstances defined by the law, including processing activities carried out in Brazil or related to individuals located in Brazil. A branch that handles employee records, customer information, vendor contacts, visitor data, or cross-border reporting may need to align global privacy policies with Brazilian legal requirements.

Good governance also requires integration between legal, tax, accounting, finance, and operations. A foreign branch can face problems when each function works in isolation. For example, a corporate amendment may be filed but not reflected in accounting records; a representative’s authority may change but internal approval workflows may not be updated; or a contract may be signed locally without adequate tax and legal review. These gaps can create operational friction and weaken the reliability of the branch’s controls.

The Brazilian Institute of Corporate Governance, known as IBGC, presents corporate governance as a system through which organizations are directed, monitored, and encouraged, involving relationships among owners, board members, management, oversight bodies, and other stakeholders. For foreign company branches, this principle is highly relevant even when the branch does not have the same governance bodies as an independent Brazilian corporation. The practical objective is the same: transparency, accountability, responsibility, and consistency in decision-making.

For headquarters, the most effective approach is to treat the Brazilian branch as part of the global governance environment while giving it the local tools it needs to operate safely. This may include a Brazil-specific compliance calendar, a delegation of authority policy, a document retention protocol, bilingual templates for corporate approvals, a third-party onboarding procedure, a periodic legal representation review, and a process for escalating regulatory or reputational risks.

The branch’s governance framework should also be reviewed whenever there is a change in business model, ownership, address, representative, tax status, strategic partner, regulated activity, or operational footprint. In Brazil, compliance is not only about avoiding penalties. It is about ensuring that the legal structure supports the business plan. When corporate governance is clear, foreign investors can make decisions faster, respond to authorities more confidently, and maintain better control over local execution.

In practice, compliance and corporate governance for foreign company branches in Brazil should be seen as a strategic foundation. A foreign branch with clear authority, updated records, reliable representation, risk-based controls, and documented decision-making is better prepared to grow responsibly. For companies entering or expanding in Brazil, the most important question is not whether governance will be needed, but whether it has been designed early enough to protect the investment from the beginning.